Average fixed mortgage rates dipped slightly last week, remaining near their all-time record lows, according to the recently released Freddie Mac Primary Mortgage Market Survey® (PMMS®).

The 30-year fixed-rate mortgage (FRM) averaged 3.43 percent with an average 0.5 point for the week ending August 18, 2016, down from the last week when it averaged 3.45 percent. A year ago at this time, the 30-year FRM averaged 3.93 percent.

The 15-year FRM averaged 2.74 percent with an average 0.5 point, down from the last week when it averaged 2.76 percent. A year ago at this time, the 15-year FRM averaged 3.15 percent.

“Ahead of the release of the FOMC minutes for July, 10-year Treasury yields were little changed from the prior week,” says Sean Becketti, chief economist, Freddie Mac. The 30-year fixed-rate mortgage fell 2 basis points to 3.43 percent this week, erasing last week’s uptick. For eight consecutive weeks, mortgage rates have ranged between 3.41 and 3.48 percent. Inflation is not adding any upward pressure on interest rates as the Bureau of Labor Statistics reported that the Consumer Price Index was unchanged in July.”Additionally, the 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.76 percent with an average 0.4 point, up from the week prior when it averaged 2.74 percent. A year ago, the 5-year ARM averaged 2.94 percent.

Tom stachler, www.LendAnnArbor.com is a great resource for the areas best lenders from a dozen different companies. Interest rates are very low at historic levels Mortgage Rate Quote, interest rates, saline, michigan, ann arbor, dexter, yspilanti, chelsea

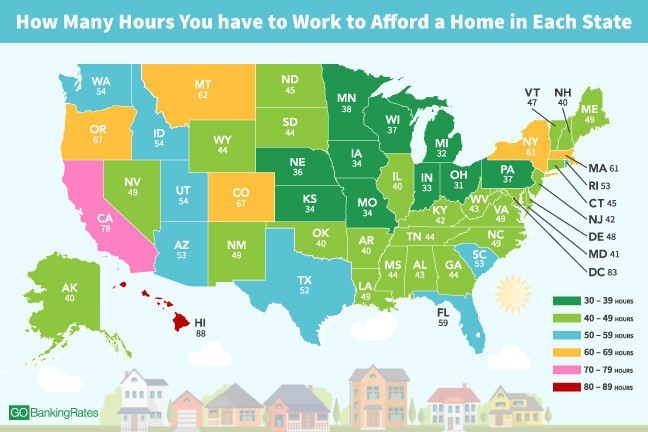

When you take your monthly mortgage payment, utility bills and other expenditures into consideration, it’s no surprise that owning a Home is an expensive proposition. But have you ever considered just how many hours you have to work to afford your home? Or how many hours you’d have to work to afford your dream home in Hawaii? (Spoiler alert: don’t buy your plane ticket quite yet!).

n fact, if you’re looking to leave the hustle and bustle of city life behind and hang 10 in Hawaii, you better be prepared to put in some long hours.

According to a study conducted by GOBankingRates—which looked at home listing prices, mortgage rates and household incomes—Hawaii tops the list of states where you’ll have to work the most to afford a mortgage, coming in at 88.13 hours a month.

On the same side of the coin are the District of Columbia (83.29 hours a month), California (78.13 hours a month) and Colorado (67.02 hours a month).

For those who can’t get enough of the great state of Ohio, you may just be in luck. The Buckeye State tops the list of places where you need to work the least to afford a mortgage at 30.76 hours a month. Next on the list is Michigan at 32.44 hours a month, Indiana at 32.72 hours a month and Iowa at 33.81 hours a month.

If you have moving on the mind, be sure to check out the infographic below before you make your decision!

For refinancing and home mortgage pre-qualification options, go to www.LendAnnArbor.com for contact information and a LIST for the area's best lenders

tom stacher, real estate, one, lowest mortgage rates, souce, financing, home, house, get the area's best lenders list, ann arbor, michigan, dexter, saline, ypsilanti, financing, condo

Self-directed IRAs that focus heavily on real estate investments are often referred to as "Real Estate IRAs." With a Real Estate IRA, your retirement funds can invest in all kinds of real estate and real estate-related assets. Explore the most popular real estate investment options for your self-directed IRA:

These are just a few of your options with a self-directed IRA. The real estate-related investments allowed in these retirement accounts are seemingly endless.

Looking for help with this type of investment, contact us today to get started with finding property and purchasing it rental or flip opportunities.

tom, stachler, thomas, real estate, one, property, income, properties, Home, houses, investment, ira, investing, using, flip, opportunities, saline, ann arbor, dexter, michigan, creative, milan, ypsilanti, michigan

John Adams Mortgage has an interesting new Program you might wish to explore. If nothing else, you get a free Amex Gift Card. See below for details and click here to Apply

Also, you can go to www.LendAnnArbor.com to get a list of the Area's best Lenders and Banks.

tom, stachler, thomas, real e

state, realty, for sale, Lease, condo, houses, homes, schools, information, ann arbor, saline, michigan, ypsilanti, mi, dexter, chelsea, brokers, realtors, reviews, finance, rates, deals, best, lender, property, listing, inventory

The Fed says it’s going to raise the overnight cost of money by about 1 percent per year for the next three years.

Mortgages in 2015 never rose above 4.25 percent nor fell below 3.75 percent; in 2016, the high-low range should be twice that.

Every day the US is more sensitive to overseas economies.

I am always reluctant to offer predictions for the year ahead because of the arrogance involved. But, shoot, as in the gallows humor of the Eighth Air Force, “No guts, no Air Medals.”

Begin with reviewing successes and embarrassments one year ago. Two mistakes: I thought the US economy would accelerate to 3 percent growth, and saw Czar Vladimir as more dangerous than he has been. Got right: The US federal government has been inert in 2015, Europe and Japan are still no-growth messes, China did slow down, the Fed did lift off from zero, but mortgage rates ended where they began. Not bad. China was the toughie last year, and is again now.

But, looking forward now, they’re all tough. China has years of dogs and horses; 2016 is going to be the Year of the Crazy. As unpredictable as any year in my memory.

In our racket, the Fed is paramount. Fed forecasting is already crazy: The Fed says it’s going to raise the overnight cost of money by about 1 percent per year for the next three years.

Financial markets growl back: No, you’re not. Wagers are set now in markets, privately and in big trades: The Fed won’t make it far above 1 percent before having to retreat. That’s an immense disagreement.

Long-term money — bonds and mortgages — thinks long term. Duh. Next year, the bond market’s view of the future is overdue for big lurches. The wrong kind of news will dramatically change the markets’ estimate of the Fed’s course and rock mortgages a quarter-percent or more over a weekend. Crazy means volatile. Look for overshoots and reversals. Mortgages in 2015 never rose above 4.25 percent nor fell below 3.75 percent; in 2016, the high-low range should be twice that.

News surprises begin with this week’s wad of December data, from Christmas sales to Friday’s employment and wage report, surprise magnified by the holiday down-time.

“The wrong kind of news….” The worst news for us would be any combination of these: accelerating gains in US wages, rising US inflation, or US jobs stubbornly gaining 200,000 or more each month. Any one of those would force markets to reconsider its Fed-doubt. Burned last year, now I think US GDP (gross domestic product) will not accelerate, but it’s those Fed-sensitive components which matter.

Crazy 2016? CRAZY!?! Donald Trump, and the other dozen all trying to flank each other on the right. Donald freakin’ Trump. Every one of them promising faster US growth, more jobs and higher wages. What’s-her-name, too. The Fed says we’re growing too fast now. Yellen: “We don’t need more than 100,000 new jobs each month.” The Fed is on track to tighten at least three times before the election. This group of candidates is not a bright lot, but do we think they won’t notice the Fed?

Do I want to see Yellen get the Trump treatment? See the Fed politicized as never before? Great.

Then look outward. Every day the US is more sensitive to overseas economies. Japan has been in deflation and recession for so long that we’re used to it. Nobody owns its bonds except itself. An exceedingly unlikely recovery might do some harm outside, but stick with exceedingly unlikely. Europe has been the biggest help holding down our rates. An unexpected recovery there would hurt, raising rates there and ending the attractiveness of our bonds, but the euro currency should prevent anything but occasional lifelike twitching.

In 2015, China took over from Europe as most important. It has slowed more than anyone thought, collapsed commodity markets and the nations exporting the commodities. China will still grow, but its growth now will be destructive to the rest of us, new money for internal stimulus sourced by predatory exports. A true revival in China would help the world and hurt rates, but that’s going to happen only via reform.

China’s reforms are stymied by internal contradiction: no one ever has found a way to modernize by repression, or to liberalize by censor, or to innovate by edict.

Be glad we’re here, crazy and all. Happy New Year!

tom stachler, real estate. one, michigan, broker, homes, for sale, Lease, property, houses, homes, mortgage, rates, future changes, china, overseas, markets, broker

There are many emotions and tough decisions that are present when selling a Home. Perhaps one of the toughest decisions involves how to price your home. While a seller never wants to price a home too low, they also don't want to price themselves out of the market. Use these four tips to setting an accurate asking price when selling your home:

Living in an age where information is available in an instant can be both a wonderful and an awful thing. Use the information available by gathering enough data to make a smart decision. Educating yourself about the selling process and local market trends, helps you elect the best asking price.

While understanding the current market is a great way to begin, it often takes seeing comparable homes to understand what asking price is appropriate for your home. Ask that your Realtor set up showings for other homes in the area so that you can see what those homes have to offer in relation to their price.

A bidding war is a seller's dream. Help to ensure multiple offers on your home by staging it effectively. Showing buyers the potential that your home has will increase the amount of offers that you receive on your home. Also be sure to sell the key features of your home. Mentioning the little touches that make life easier goes a long way in securing offers.

Selling a home is an emotional time. When pricing a home, it is important to take your emotions out of the process. Buyers are not interested in paying you for the sentimental value of the home. They only want to secure the perfect home at a fair price.

These four tips to setting an accurate asking price will hopefully provide you with the information that you need to make a decision about the selling price of your home. It is important to remember that your real estate agent is someone that possesses the information to assist you through every step of the process, including determining an accurate asking price. Rely on their experience during this difficult decision.

There are numerous reasons that help to cultivate bidding wars. One of the most common is when the market has fewer homes than interested buyers. This increased competition doesn't mean that you can't get the Home of your dreams. Winning a bidding war is easy when armed with these helpful tips:

Being prepared is the best strategy when trying to win a bidding war. This includes having your financing ready. Sellers are more likely to accept an offer that is backed by a preapproval letter. Since preapproval can take a while, having accomplished that step is appealing to the seller.

Be sure to avoid making lowball offers. In the case of a bidding war, low offers aren't considered to be serious offers and are rejected immediately. If the home is out of your price range, keep it off of your list. In a competitive market, placing an offer on a home that is out of your range only wastes time and leads to disappointment.

Money isn't the only thing that makes an impression during a bidding war. Flexibility can go a long way towards having your offer selected. That flexibility can be shown by offering the buyers preferred move-out date or by the willingness to waive the small items that come up during an inspection.

While you may not be able to offer much more than the asking price of the home, using your cash creatively can help your bid win. This could be offering more earnest money than required or offering a larger down payment that necessary. Both of those items can be appealing to sellers.

While a bidding war is a dream for a seller, it can be a nightmare for the buyers involved. Winning a bidding war seems like a daunting task, but is actually something that is very possible when the buyers go in with all of the necessary information.

There is some good news for individuals who are currently trying to sell their Home. According to recent statistics, home sales are now the strongest they've been in the last seven years. While the national real estate market has clearly gone through some tough times since the 2008 recession began, there is some pent-up demand for home sales that is fueling a slow but steady recovery. Record low interest rates and a slight rise in resales this past December show that those who are currently trying to sell a property have a considerable chance at finding a buyer in the coming months.

Home sales in 2013 show that home sales of existing homes have been the strongest in 7 years, which is bringing some optimism to the real estate industry as a sign that the market is gaining health. Home resales rose through December, as was expected according to a poll of economists given by Reuters earlier in 2013. Although resales had gone down due to increases in the interest rates of mortgages, there has been some new development activity among builders that shows that the demand for properties is out there despite multi-decade lows in household formation.

The obstacles that the housing market still faces include rising prices in combination with the fact that incomes do not seem to be growing proportionally across the country. Despite the fact that home sales were the strongest in 2013 that they have been in seven years, the median price for an existing home has risen alarming– by almost 10 percent– between December of 2012 and December of 2013.

The rise in home prices can be attributed to the fact that there is a shortage of available homes on the market. Due to market uncertainty, many homeowners who would otherwise put their homes up for sale are reluctant to attempt to find a buyer. The number of unsold properties on the market has fallen significantly over the last few months, and scarcity in available prices is contributing to rises in home values.

However, the pick-up in the market that was shown in 2013 will hopefully continue and encourage would-be sellers to put their homes up for sale. Ideally, this will lead to a stabilization of home prices across the country.

Fannie Mae recently announced an expansion of it's Homepath Mortgage product that provides Home buyers and investors financing for the purchase of any Fannie Mae-owned property.

The new product will soon allow eligible individual and LLC borrowers the option to finance up to 20 properties using the Homepath Mortgage. Our Realtor association, NAR has long called for the expansion of financing opportunities for investors as a way to increase the absorption of REO properties.

Fannie Mae will offer flexible lending terms and will not require appraisals of the properties. Contact us today for assistance in the acquisition of Residential or Commercial Income properties. I have field work sheets to help you determine the bottom line returns. (NOI or Net Operating Income) and 35 years of experience in the income property business.

Click the link above for Investor Income property Inventory Results under "All MLS Listings"